Investor Overview

Investors

Access our latest announcements, results, share price information and other resources here

CV Standalone Financials: Focus on profitable growth drives robust financial results

Q4: Revenue ₹24.5K Cr (+22%), EBITDA at ₹3.4K Cr (+35%), PBT (bei) ₹3.0K Cr (up ₹1,089 Cr)

FY26: Revenue ₹77.4K Cr (+11%), EBITDA at ₹10.2K Cr (+22%), PBT (bei) ₹8.7K Cr (up ₹2,721 Cr), FCF ₹9.2K Cr (up ₹2.2K Cr)

Mumbai, May 13, 2026: Tata Motors Ltd. (TML) announced its results for quarter and year ending March 31, 2026.

Summary:

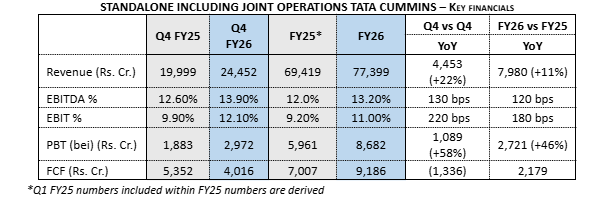

Tata Motors Standalone delivered a record Q4 FY26 performance and a strong full year, underpinned by disciplined execution and focus on profitable growth. Quarterly revenue stood at ₹24.5K Cr (+22%), with EBITDA at ₹3.4K Cr (+35%). The Company achieved teens EBITDA margin at 13.9% (+130 bps), ahead of its mid-term guidance. EBIT margin expanded to 12.1% (+220 bps), aided by higher volumes, improved realizations and continued cost efficiencies, partially offset by higher input costs. PBT (bei) for the quarter stood at ₹3.0K Cr (+58%). Profit after tax for the quarter was ₹2.4K Cr (+70%). For the full year FY26, revenue stood at ₹77.4K Cr (+11%), with EBITDA of ₹10.2K Cr (+22%) and EBITDA margin at 13.2% (+120 bps). EBIT margin for FY26 stood at 11.0% (+180 bps). PBT (bei) for the full year came in at ₹8.7K Cr (+46%). Profit after tax for the year was ₹3.4K Cr (-23%) including the impact of ₹3.7K Cr on account of exceptional items pertaining to Mark-to-Market losses on account of listed investments in Tata Capital, New Labor Code, demerger related costs etc.

Strong operational performance and efficient working capital management through the year resulted in consistent growth in full year Free Cash Flow of ₹9.2K Cr (+₹2.2K Cr). Net cash for the domestic business stood at ₹7.5K Cr as of March 31, 2026. The Company's disciplined approach to capital allocation has led to an industry-leading Auto ROCE of 72% in FY26 (vs. 61% in FY25).

Consolidated financials: Consolidated revenues for Q4 FY26 stood at ₹26.1K Cr (+19%). EBITDA margin stood at 13.1% (+150 bps) while EBIT margin came in at 11.5% (+230 bps). PBT (bei) for the quarter was ₹2.4K Cr (+29%) and Profit after tax stood at ₹1.8K Cr (+35%). As at March 31, 2026, the Company was Net Cash positive at ₹13.7K Cr. This included TMF Holdings gross debt less market value of TMF Holdings investments in Tata Capital Ltd.

For the full year FY26, consolidated revenues stood at ₹83.9K Cr. EBITDA margin was 12.3% and EBIT margin was 10.2%. Full year PBT (bei) was ₹6.1K Cr (+7%) while Profit after tax stood at ₹3.0K Cr (-24%), including the impact of ₹1.4K Cr. on account of exceptional items pertaining to New Labor Code, demerger related costs etc.

Dividends: The Board of Directors has recommended a final dividend of ₹ 4/- per share subject to approval by the shareholders.

Corporate Actions:

Iveco update: The regulatory approvals for the proposed acquisition of Iveco are currently underway with most of the approvals already received. Last pending approvals are being actively pursued for the earliest closure. Given this, Tata Motors expects to complete the transaction by Q2 FY27.

Business Highlights for the year:

Girish Wagh, MD & CEO, Tata Motors Ltd said:

“FY26 marked a clear inflection point for the commercial vehicles industry, with volumes surpassing the pre-FY19 peak, supported by GST 2.0 reforms and sustained infrastructure spending. For Tata Motors Commercial Vehicles, FY26 was a landmark year as we delivered milestones of revenues and profits and reinforced industry leadership and strengthened our market position. Looking ahead, the underlying demand fundamentals remain resilient despite geopolitical uncertainties signaling some moderation in the near term. With strong business fundamentals, proactive risk mitigation, disciplined execution and a refreshed portfolio offering industry-leading TCO and smart digital solutions, we remain agile and well positioned to sustain momentum through customer-centric solutions to create long-term stakeholder value.”

GV Ramanan, CFO, Tata Motors Ltd. said:

“FY26 marked a strong financial performance with robust EBITDA, profit and free cash flow. EBITDA margins in Q4 FY26 crossed ‘teens’ at 13.9% while full year FCF translated to ~12% of revenue, well ahead of our 2027 target. These deliverables reflect sustained structural improvements and efficient capital and cost management. Our robust cash position gives us the flexibility to pursue disciplined capital allocation while continuing to deliver meaningful returns to shareholders. While near term headwinds including commodity cost pressures are expected to persist, we remain confident in our ability to navigate these challenges through operational efficiency, pricing discipline, and proactive supply chain management.”

ADDITIONAL COMMENTARY ON FINANCIALS (CONSOLIDATED NUMBERS, IND AS)

Finance Costs dropped to ₹166 Cr in Q4 FY26 vis a vis ₹319 Cr in Q4 FY25.

Free Cash Flow for the quarter and full year FY26 was at ₹8.0K Cr and ₹12.4K Cr respectively (including advance received for Indonesia order) vis a vis ₹5.3K Cr in Q4 FY25 and ₹5.9K Cr in FY25. Net cash as at 31st March 2026 was ₹13.7K Cr (including leases ₹798 Cr).

CV Standalone Financials: Focus on profitable growth drives robust financial results

Q4: Revenue ₹24.5K Cr (+22%), EBITDA at ₹3.4K Cr (+35%), PBT (bei) ₹3.0K Cr (up ₹1,089 Cr)

FY26: Revenue ₹77.4K Cr (+11%), EBITDA at ₹10.2K Cr (+22%), PBT (bei) ₹8.7K Cr (up ₹2,721 Cr), FCF ₹9.2K Cr (up ₹2.2K Cr)

Mumbai, May 13, 2026: Tata Motors Ltd. (TML) announced its results for quarter and year ending March 31, 2026.

Summary:

Tata Motors Standalone delivered a record Q4 FY26 performance and a strong full year, underpinned by disciplined execution and focus on profitable growth. Quarterly revenue stood at ₹24.5K Cr (+22%), with EBITDA at ₹3.4K Cr (+35%). The Company achieved teens EBITDA margin at 13.9% (+130 bps), ahead of its mid-term guidance. EBIT margin expanded to 12.1% (+220 bps), aided by higher volumes, improved realizations and continued cost efficiencies, partially offset by higher input costs. PBT (bei) for the quarter stood at ₹3.0K Cr (+58%). Profit after tax for the quarter was ₹2.4K Cr (+70%). For the full year FY26, revenue stood at ₹77.4K Cr (+11%), with EBITDA of ₹10.2K Cr (+22%) and EBITDA margin at 13.2% (+120 bps). EBIT margin for FY26 stood at 11.0% (+180 bps). PBT (bei) for the full year came in at ₹8.7K Cr (+46%). Profit after tax for the year was ₹3.4K Cr (-23%) including the impact of ₹3.7K Cr on account of exceptional items pertaining to Mark-to-Market losses on account of listed investments in Tata Capital, New Labor Code, demerger related costs etc.

Strong operational performance and efficient working capital management through the year resulted in consistent growth in full year Free Cash Flow of ₹9.2K Cr (+₹2.2K Cr). Net cash for the domestic business stood at ₹7.5K Cr as of March 31, 2026. The Company's disciplined approach to capital allocation has led to an industry-leading Auto ROCE of 72% in FY26 (vs. 61% in FY25).

Consolidated financials: Consolidated revenues for Q4 FY26 stood at ₹26.1K Cr (+19%). EBITDA margin stood at 13.1% (+150 bps) while EBIT margin came in at 11.5% (+230 bps). PBT (bei) for the quarter was ₹2.4K Cr (+29%) and Profit after tax stood at ₹1.8K Cr (+35%). As at March 31, 2026, the Company was Net Cash positive at ₹13.7K Cr. This included TMF Holdings gross debt less market value of TMF Holdings investments in Tata Capital Ltd.

For the full year FY26, consolidated revenues stood at ₹83.9K Cr. EBITDA margin was 12.3% and EBIT margin was 10.2%. Full year PBT (bei) was ₹6.1K Cr (+7%) while Profit after tax stood at ₹3.0K Cr (-24%), including the impact of ₹1.4K Cr. on account of exceptional items pertaining to New Labor Code, demerger related costs etc.

Dividends: The Board of Directors has recommended a final dividend of ₹ 4/- per share subject to approval by the shareholders.

Corporate Actions:

Iveco update: The regulatory approvals for the proposed acquisition of Iveco are currently underway with most of the approvals already received. Last pending approvals are being actively pursued for the earliest closure. Given this, Tata Motors expects to complete the transaction by Q2 FY27.

Business Highlights for the year:

Girish Wagh, MD & CEO, Tata Motors Ltd said:

“FY26 marked a clear inflection point for the commercial vehicles industry, with volumes surpassing the pre-FY19 peak, supported by GST 2.0 reforms and sustained infrastructure spending. For Tata Motors Commercial Vehicles, FY26 was a landmark year as we delivered milestones of revenues and profits and reinforced industry leadership and strengthened our market position. Looking ahead, the underlying demand fundamentals remain resilient despite geopolitical uncertainties signaling some moderation in the near term. With strong business fundamentals, proactive risk mitigation, disciplined execution and a refreshed portfolio offering industry-leading TCO and smart digital solutions, we remain agile and well positioned to sustain momentum through customer-centric solutions to create long-term stakeholder value.”

GV Ramanan, CFO, Tata Motors Ltd. said:

“FY26 marked a strong financial performance with robust EBITDA, profit and free cash flow. EBITDA margins in Q4 FY26 crossed ‘teens’ at 13.9% while full year FCF translated to ~12% of revenue, well ahead of our 2027 target. These deliverables reflect sustained structural improvements and efficient capital and cost management. Our robust cash position gives us the flexibility to pursue disciplined capital allocation while continuing to deliver meaningful returns to shareholders. While near term headwinds including commodity cost pressures are expected to persist, we remain confident in our ability to navigate these challenges through operational efficiency, pricing discipline, and proactive supply chain management.”

ADDITIONAL COMMENTARY ON FINANCIALS (CONSOLIDATED NUMBERS, IND AS)

Finance Costs dropped to ₹166 Cr in Q4 FY26 vis a vis ₹319 Cr in Q4 FY25.

Free Cash Flow for the quarter and full year FY26 was at ₹8.0K Cr and ₹12.4K Cr respectively (including advance received for Indonesia order) vis a vis ₹5.3K Cr in Q4 FY25 and ₹5.9K Cr in FY25. Net cash as at 31st March 2026 was ₹13.7K Cr (including leases ₹798 Cr).

Access our latest announcements, results, share price information and other resources here